How I bought my first house on a $47000 per year salary

Buying a home can seem like such a daunting and overwhelming endeavor. This is because mortgage financing and real estate lingo often sounds so foreign and the price tags of houses, given that a house is usually the most expensive purchase a person will make in his or her lifetime, can lead to legit sticker shock.

After finishing my Pediatric Residency at Boston Children’s Hospital in the summer of 2008, I was bound for Baltimore to continue my post-graduate medical training in Anesthesia and Pediatric Critical Care at Johns Hopkins Hospital. I was going to be starting as a Resident in Anesthesiology with a $46500 per annum salary. Given that I had signed up for a second residency and two fellowships at Hopkins, I was committed to living in Baltimore for at least 5 years. It did not make sense to me to keep paying rent for all those years, however, concerns lingered in my mind–could I really afford to buy a house on my salary? Would I qualify for a mortgage and how could I come up with the down payment in the first place? As a single woman at the time, would I be able to keep up with the type of maintenance a house would require? Also, keep in mind that 2008 was the year of the housing market crash, so there were tons of examples all around me of people who bit off more than they could chew in home buying and were now financially devastated by foreclosures or short sales, lost homes and damaged credit. I did not want to become a statistic.

I knew, however, that buying a house would lead to some tax advantages for me, so I decided to explore the possibilities–I dared to dream. I ended up buying a 3 bedroom 2.5 bathroom house with a partially finished basement in the Ednor Gardens community in Baltimore (near the Johns Hopkins University (Undergraduate) Campus. The price was $215000. I lived in that house for 6 years. During my time in that house, I planned my wedding, I got married, I lost my father, I gave birth to my first son and I completed my extensive medical training. Through it all, I enjoyed many years of home-owner tax credits. I still own the house as a rental property. Even though the Baltimore housing market crashed further later in 2008, I am still so glad I decided to take on home ownership as I bought at a time when prices were already on their way down, so my gains still outweigh my losses.

So here are some important lessons/pieces of advice/nuggets of wisdom that I picked up along my first home-buying journey that you may find helpful:

- Create a monthly budget and learn to live by that budget: You need to have a clear understanding of your monthly expenses in order to make accurate projections about what you can afford in monthly mortgage, home insurance, real estate tax and maintenance budget payments. Your home payments (mortgage+home insurance+real estate tax+monthly maintenance savings) should be 1/3rd or less of your monthly NET income. So create a detailed list of your monthly expenses from hair treatments to cell phone bills to pedicures, create realistic estimates based on your previous spending habits and live by that budget.

- Start saving money (if you haven’t already): If you are used to blowing your monthly budget and living check to check, look for areas where you can trim your budget in order to save money for rainy day spending and money for your down payment. For example, I got a hair style that I could maintain easily myself, I cut down on eating out and shopping for things I did not need (clothes, shoes etc) and I started shopping smarter (looking for sales, discounts and deals).

- Consider getting a 2nd job (or additional source of income): I got two moonlighting gigs in the hospital I worked in as a Pediatric Resident. As Residents, we were restricted to working 80 hours per week only (yes, that is a restriction…LOL!) So during the few weeks where I was under 80 hours per week, I would work extra shifts in the Emergency Room, the Pediatric ICU or in the Neonatal ICU to make up to 80 hours per week. I saved all the money from my moonlighting gigs.

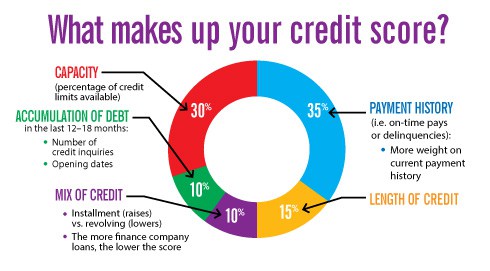

- Know your Credit Score and learn about Credit: A credit score of 660 is considered to be a good Score. Your Credit Score will determine the interest rate for which you will qualify. For example, today a Credit Score of 600 will mean an interest rate of 4.375% versus a Credit Score of 700+ an interest rate of 3.75% (this is can mean a difference of 100s of dollars a month in monthly mortgage payments. When you are within 6 months of purchasing a home, you need to speak to a Mortgage Specialist at that point to create a plan for your credit profile. DO NOT do this by yourself or with advice from your Uncle Felix (trust me on this one).

- Income versus Debts: Understand that the most important thing is not how much money you make but what your current debts are in relation to your income. With my $47000 salary, I had only 1 credit card and it was fully paid off, my medical school loans (which had been consolidated to 2.5% interest rate and deferred) and a car note that had only 1 year left. You can have a great six-figure salary but if you are riddled with loads of debt, you may have more challenges than someone with a five-figure salary who has minimal debt.

- Contact a Mortgage Professional/Specialist: A Mortgage Professional will go over your budget, assess your credit profile and overall financial situation, and discuss down payment options. For those who need credit score improvement to qualify for a loan or to obtain a better interest rate, your Mortgage Professional should assist you in creating a plan to improve your credit core (e.g. picking out which specific payments to make that will have the best bang for your buck with boosting your credit score).

Often times, people will try to work on their credit scores independently which is a very bad idea. You will achieve a better result if guided by a Mortgage Professional as this is their area of expertise. They are not there to judge you. These are professional experts who want to help you succeed in purchasing a home. Your success is their financial gain so it will be a mutually-beneficial relationship. Your Mortgage Professional will also know all the rules of the game, potential pitfalls, the lending requirements as well as the best mortgage tools and will combine that knowledge with having your best interest at heart. I used Mary Levinson who is a 17 year Real Estate veteran and a branch manager of a Mortage Company, NFM Lending. NFM Lending is a national lender that is licensed in 30 states in the United States.

- Build a Home Buying Team: Real Estate Agent + Mortgage Specialist + Buyer (in the state of Massachusetts the Buyer has to employ a Lawyer directly as well). The Real Estate Agent and Mortgage Specialist will work together to ensure that you get the right home at the right price and the best mortgage package possible. You need an experienced real estate agent that understands local home buying/selling trends, mortgages, home maintenance details and home inspection.

- Down Payment: You will likely not have the 20% down payment that is needed for traditional mortgages unless you are independently wealthy, come from money or living rent free (for whatever reason) and able to save up most of your income. I didn’t have 20%–which for my $215000 house would have been $43000 (essentially my gross annual salary at the time). So, how was I able to buy a house? Enter FHA: Federal Housing Administration Loan. FHA Loan qualification is a Government-insured loan that most banks provide. It is more forgiving about credit scores, and offers the lowest interest rates with the lowest down payment option. According to Mortage Specialist Mary Levinson, most first time home buyers will take advantage of the FHA loan option (about 80%). FHA requires 3.5% down payment: For my $215000 home, that was $7525. I ended up putting down $10000.

- Crunch the Numbers: For a $200000 home with an interest rate of 3.875% (Credit Score 660)–your monthly payment (mortgage over 30 years + Home Owners Insurance + Property Taxes + Mortgage Insurance) will be about $1500 per month.

Here is the break down: FHA 3.5 % Down Payment: $7000; loan amount $193000 (total $200000)

Principle + Interest Rate (over 360 months): $923 per month

Home Owners Insurance: $75 per month

Property Taxes (Baltimore City): $275 per month

Mortgage Insurance (this is added because you do not put down 20% down payment): $139 per month

Total: $1412 per month (approximately $1500)

*$1500 was less than what I would pay in monthly rent for a 1 bedroom apartment.

**Please NOTE: First time homebuyers are not limited to purchasing a $200000 home–you can buy up to $650000 using FHA loan options depending on the state and county in which your are purchasing. In Baltimore County, I could have purchased up to a $525000 home.

- Understand the advantages of home ownership: Why buy a home? Why not just rent? The time to buy is when you know you will be in a particular place for 3+ years as a minimum. I was going to be in Baltimore for 5 years at least.

Comparing renting versus paying a mortgage: Renting for $1500 per month for 3 years ends up being $54000 in rent as money to your Landlord. If you bought the $200000 home and put down $7000 down payment using an FHA loan option, over 3 years of mortgage payments, you would actually be saving $88 per month ($1500-$1412 = $88) plus you would have gained equity in the home (an investment for you) + tax benefits for mortgage interest tax deductions that you can claim yearly on federal tax returns = Larger Tax Refund. Home ownership basically reduces your tax burden because the government essentially incentivizes home buying. As a single, childless, head of household at the time–that was music to my ears!!!

I would love to hear your thoughts on this topic, as well as any suggestions that you may have. Please share them in the comment section below and let’s grow together, building a strong community of lifelong learners.

Love, Chichi

I struggled with home ownership in bmore and had many of the same fears. Didnt purchase myself, but started to take steps towards it and had a bad experience . Agree with the tax benefit and money savings. Overall great info. Love the way you broke it down!

I totally understand. It can be scary and sometimes, bad things happen to good people; that is why I wanted to break things down as much as possible, demystify the process and arm people with helpful information. Please share with folks who you think may benefit from this. Thanks so much for the feedback.

Chichi, I really, really appreciate this! This is good math and the break down is so clear! I definitely took some written notes. Thank you!

Wow! Your feedback has made my day. This moment is literally one of the main reasons I started this blog. Glad to be of help dear. Please reach out anytime if you have further questions. Cheers and thank you for the feedback.

Chichi, great information. I’m starting late in life wanting to purchase a home. So I’m sure my challenges will be somewhere different but still the same I would be a first time home buyer. Hearing your story gives me courage to go ahead and start my budget right now. I am no longer afraid. Grateful!!

Wow Phyllis! I am so glad to hear this. I am so glad that you found this post helpful. You can definitely do this! There are also special programs available to first time home buyers. Please reach me at chichichicmd@gmail.com as I have recommendations for a top class real estate agent and the best real estate lawyer that can help you avoid pitfalls. All the best in your journey. Love, Chichi 🥰

Hello to all wow thanks so much for sharing your experiences.

I’m on $48,000 and I’m pursuing to purchase a home I’m miami Florida. As a mother of 4 I’m

Not going to lie a lot of people tell me is not as easy as it seems however others tell me is great for me to look into purchasing a house.

I won’t lie I’m kind of scared but I’ve lived for so many years with this fear of purchasing. Now at 42 I do believe I’m ready to move forward

Looking to to buy within 6 months from now I’m aware I will have to be very disciplined with my expenses.

I can’t work. Second job I mean I don’t want to sacrifice not being with my twins . I do appreciate the feed back .

I know I will have to be responsible for all of the maintenance and insurance on the home as well as the taxes Pay yearly .

I pray next time I get on here I’m a first time home owner.

Thank you all

Thank you so much for reading the post. I do pray that you become a first time home owner by the time you next check my blog out again. If you are not able to get a second job (yes! spending time with your twins is waaaaaaaay more important), then you may have to focus more on being as efficient with your expenses as possible. Hopefully you can get an area that has good schools and not too crazy taxes. I did my best to learn certain maintenance skills on youtube and only outsourced the big projects. Please let me know if you have any questions I can help answer (chichichicmd@gmail.com or DM me on Instagram).